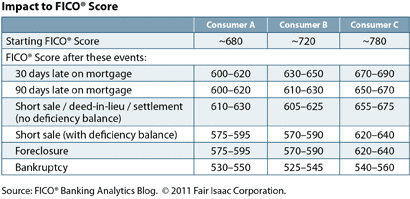

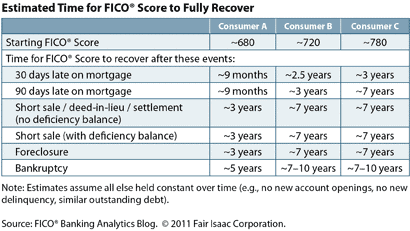

You have several different options for dealing with a home that’s worth less than what you owe on it, two of which are foreclosure and a short sale. One common justification that realtors give for pushing a short sale is that it’s better on your credit score. However, according to research by the authors of the FICO Banking Analytics Blog, that may not be the case.

Short sales are placed into two categories – those which result in a deficiency, and those that do not. A deficiency occurs when the lender does not agree to forgive the difference between what the home sells for in the short sale and what you owe on the debt. As is clear from the following chart, if your short sale leaves a deficiency it’s impact on your credit and your recovery is the same as a foreclosure.

Given that the effect on credit is comparable, an valuable alternative to a short sale is foreclosure with a strategically filed chapter 7 bankruptcy. If done by an experienced bankruptcy lawyer, this technique can result in families remaining in their homes for a year or more after making the last mortgage payment and walking away with a fresh start.

If you’re underwater on your home, schedule a free consultation with a debt relief attorney to learn about all of your options and not just those that benefit the mortgage company or the realtor trying to sell you a short sale.